Operations Planner

« »

| S | M | T | W | T | F | S |

|---|

| | 1 | 2 | 3 | 4 | 5 |

| 6 | 7 | 8 | 9 | 10 | 11 | 12 |

| 13 | 14 | 15 | 16 | 17 | 18 | 19 |

| 20 | 21 | 22 | 23 | 24 | 25 | 26 |

| 27 | 28 | 29 | 30 | |

|

Hotel Managers Labor To Control Labor

publication date: May 21, 2012

|

author/source: Robert Mandelbaum

Hotel Managers Labor To Control Labor

By: Robert Mandelbaum,

2012

Coming out of lodging industry recessions, we have historically observed fairly significant increases in hotel operating expenses. Since the initial revenue recovery is typically driven by occupancy, variable expenses naturally rise with the increased volume of rooms occupied and guests served. In addition, hotel managers desire to reinstate the services and amenities that were discontinued during the downturn contributes to above-average expense growth.

On the revenue side, the industry recovery observed in 2010 was "typical". In aggregate, the participants in PKF Hospitality Research's (PKF-HR) 2011 Trends® in the Hotel Industry survey saw their rooms revenue (RevPAR) rise 5.3 percent, the result of a 6.2 percent increase in the number of rooms occupied and a 0.9 percent decline in average daily room rate (ADR). One would expect such an imbalance of occupancy and ADR to cause a sharp rise in operating expenses, but that was not that case. The "atypical" trend we observed in 2010 was a very modest 3.4 percent increase in total hotel operating costs.

Labor Is Costly

When analyzing hotel expenses, labor costs (inclusive of salaries, wages, bonuses, and payroll-related expenditures) are usually the first item to be examined since they are the largest expense. Since 1960, unit-level labor costs have averaged 43.7 percent of total hotel operating expenses and have increased at an average annual rate of 4.3 percent. This compares to an average annual increase of 4.0 percent for all other operating expenses combined.

Changes in hotel labor costs are also extremely volatile. From 1960 to 2010, the standard deviation for the annual changes in unit-level hotel labor costs was 4.2 percent. During this time period the annual changes in hotel labor costs swung from a high of positive 12.3 percent to a low of negative 10.4 percent.

Labor Is Controllable

Despite the challenges, hotel operators do adjust their staffing and payrolls according to changes in business volumes. Over time, labor costs measured as a percent of total revenue fall in a very tight range of 30 to 35 percent. This indicates that managers will react to changes in revenue.

It was management's ability to control labor costs that resulted in only a modest rise in total operating expenses during 2010. From 2009 to 2010, hotel labor costs increased 2.7 percent. This is well below the long run average. For comparison purposes, all other operating expenses grew by 5.3 percent in 2010, significantly above the long run average for this measure.

Controlling Factors

We attribute management's ability to control labor costs in 2010 to three main factors: increased productivity, controlling employee benefits, and persistent high levels of unemployment.

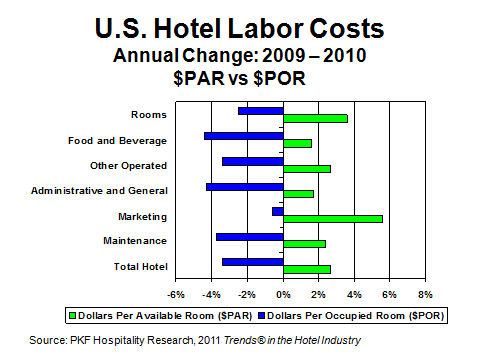

Concurrent to the 2.7 percent rise in labor costs from 2009 to 2010 was a 6.2 percent increase in the number of rooms occupied. Therefore, when measuring labor expenditures on a dollar per-occupied-room (POR) basis they declined by 3.4 percent, indicative of enhanced employee productivity. For example, in the rooms department with a great amount of variable staffing (desk clerks, room attendants, bell staff, laundry), labor costs increased 3.6 percent on a dollar per-available-room (PAR) basis, but declined by 2.5 percent on a POR basis.

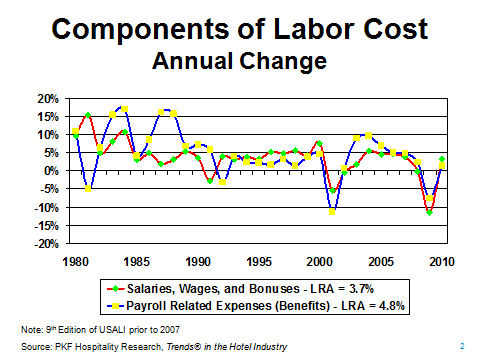

Historically it has been the payroll-related expenses (USALI vernacular for benefits) portion of labor costs that has concerned hotel operators. For the most part, hotel management can adjust hours, wages rates, and salary levels. However, a large component of payroll-related expenses (taxes, health benefits) is government mandated, thus less controllable.

In 2010, hotel managers were successful in bucking this trend. During the year, salaries, wages, and bonuses increased by 3.2 percent. Meanwhile, the payroll-related component of compensation grew by just 1.4 percent.

According to an October 3, 2011 article in the Wall Street Journal, Marriott International has instituted a policy that allows hourly staffers to take, "paid time off in shorter, part-day increments, so they can manage doctor or school appointments without having to take an entire day off." In an October 5, 2011 HotelNewsNow.com article, Michelle Russo of Hotel Asset Value Enhancement commented on recent practices she has observed among management companies. In addition to cuts in executive committee salaries and changes in incentive calculations, she had seen management companies freeze their 401K contributions. However, as market conditions have improved in 2011, Ms. Russo warns that more managers are achieving their incentive bonuses, thus causing a rise in payroll costs. In addition, 401K matching is being reinstated and pushing year-over-year increases in benefit expenses.

The persistent high levels of unemployment have suppressed the pressure on all business owners to raise wages rates and salaries. Unemployment levels have been the highest among people with the least educational experience and lowest levels of income. This is particularly pertinent in the lodging industry which offers a high percentage of low-skilled, line-level positions.

Looking Forward

Several indicators point towards a continuation of relatively low increases in hotel labor costs in the future. As of September 2011, the Bureau of Labor Statistics is forecasting total compensation for all private industries to increase at an average annual rate of 2.4 percent from 2011 through 2015. This is less than the 4.0 percent long-run average for this measure. Further, most economic forecasters are projecting continued high levels of unemployment among the traditional labor pool for line-level hotel employees.

Randy Pullen, president of WageWatch, Inc., noted in an October 16, 2011 article on HotelsMag.com that he has already seen hotel operators report a roll back in the labor cost increases that hoteliers were initially expecting for 2011. In November of 2010, 2,400 hotels had reported to WageWatch that they budgeted for a 2.9 percent average increase in hourly and salaried compensation for the upcoming year. Through October 2011, WageWatch survey participants were reporting that actual labor cost increases for the current year have materialized at an annual rate of just 1.4 percent. Staffing levels may be up due to the increase in occupancy, but the salary and wage component of labor costs still appears to be under control.

According to the December 2011 edition of Hotel Horizons®, PKF-HR is forecasting extremely low levels of new supply, along with above-average increases in demand and ADR through 2015. The net result will be annual RevPAR gains ranging from 6.1 to 7.4 percent through 2014. The ability of hotel managers to control labor costs will be a major contributing factor enabling revenue gains to translate into double-digit annual growth in profits.

Robert Mandelbaum is the Director of Research Information Services for PKF Hospitality Research. He is located in the firm's Atlanta office. For more information on PKF-HR benchmarking reports, please visit www.pkfc.com/store. This article was published in the December 2011 issue of Lodging.

|

. Contact: Robert Mandelbaum

Director of Research Information Services

Colliers PKF Hospitality Research

3475 Lenox Road

Suite 720

Atlanta, GA 30326

404-842-1150, ext 223 (Direct)

404-842-1165 (Fax)

robert.mandelbaum@pkfc.com

www.pkfc.com

Labor Is Costly

When analyzing hotel expenses, labor costs (inclusive of salaries, wages, bonuses, and payroll-related expenditures) are usually the first item to be examined since they are the largest expense. Since 1960, unit-level labor costs have averaged 43.7 percent of total hotel operating expenses and have increased at an average annual rate of 4.3 percent. This compares to an average annual increase of 4.0 percent for all other operating expenses combined.

|

|